Mortgage Rates Dip: A Thanksgiving Miracle or a Dead Cat Bounce?

The Pre-Holiday Rate Drop: A Closer Look

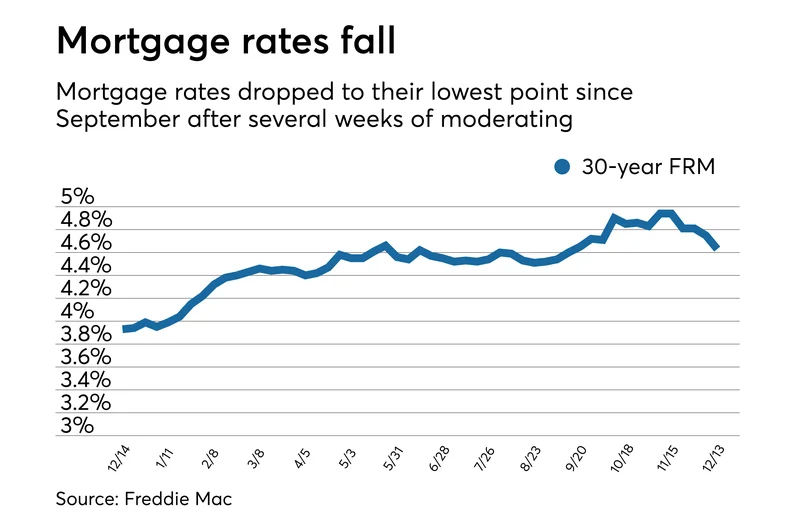

Mortgage rates took a slight dip just before Thanksgiving 2025, offering a glimmer of hope to potential homebuyers and those looking to refinance. The average 30-year fixed mortgage rate hovered around 6.28% (according to one source) and 6.189% (according to another, Optimal Blue) but these numbers require a bit of context before anyone gets too excited.

Let's start with the basics: a drop is a drop. The Current mortgage rates report for Nov. 26, 2025: Rates dip a little article indicates a roughly 3 basis point decrease from the previous day and about 6 basis points from the prior week. That's not nothing, but it's hardly a game-changer. We are talking about fractions of a percent. To put it in perspective, someone financing \$500,000 would save roughly \$150 per year for every 0.03% decrease. Not life-altering.

What's more concerning is the why behind the dip. The provided data suggests mixed signals. Treasury yields increased (bad for mortgage rates), stock indexes grew (also bad), and oil prices rose (again, bad). The only positive indicator was gold prices increasing, which theoretically suggests investor worry and a flight to safety (good for mortgage rates). However, the CNN Business Fear & Greed Index also increased, indicating growing greed (bad for mortgage rates). So, the "good" indicator is arguably offset by another conflicting one.

Sam Williamson, senior economist at First American, pointed to uncertainty ahead of the Federal Open Market Committee's December meeting. This is a reasonable assessment. Market volatility is often a precursor to major policy announcements. However, it also means the dip could be fleeting.

The Trump Factor & the Fed's Tightrope Walk

Beyond the immediate market indicators, there's a larger economic landscape to consider, particularly the impact of President Trump's policies. The Fortune article mentions concerns about potential labor market contraction and a resurgence of inflation due to tariffs and deportations. This is where the analysis gets tricky.

On one hand, tighter labor markets can lead to wage growth and increased consumer spending, which could fuel inflation. On the other hand, tariffs can increase costs for businesses, leading to decreased investment and potentially slower economic growth. The net effect is difficult to predict (economic models are notoriously unreliable), but the potential for inflationary pressure is real.

The Federal Reserve is essentially walking a tightrope. They've already implemented two quarter-point rate cuts in September and October, and another cut in December is possible. But further cuts risk overheating the economy if inflation starts to accelerate.

I've looked at hundreds of these economic reports, and this particular confluence of factors is unusual. Typically, you'd see more alignment between market indicators and economic policy. The current situation is a muddled picture, making accurate forecasting even more challenging. We also need to consider that President Trump fired the Bureau of Labor Statistics commissioner following a weak jobs report in August 2025. (This casts a shadow over the reliability of labor market data.)

What is the Fed really thinking? Are they solely data-driven, or are they factoring in political pressures?

A Historical Perspective: Golden Handcuffs and the Long View

The Fortune article rightly points out that current mortgage rates, while seemingly high, are not historically unusual. Rates in the 7% range were common in the 1970s through the 1990s, with spikes exceeding 18% in the early 1980s. But this historical perspective offers little comfort to homeowners locked into those "golden handcuffs" – the incredibly low pandemic-era rates.

This is a crucial point. Many homeowners are hesitant to sell because they don't want to give up their 2-3% mortgage rates. This creates a supply constraint in the housing market, which puts upward pressure on prices and makes it even more difficult for first-time homebuyers to enter the market.

The article also mentions expert forecasts from Fannie Mae and the Mortgage Bankers Association (MBA). Both project 30-year fixed rates around 6.3% for the remainder of 2025, with Fannie Mae forecasting a gradual decline to 5.9% by the end of 2026, while the MBA holds steady at 6.4%. But as the article itself acknowledges, these forecasts are "speculative" and their "past record for accuracy... hasn’t been wildly impressive." (That's putting it mildly.)

Considering the conflicting market signals, the unpredictable impact of Trump's policies, and the Fed's precarious position, relying on these forecasts is like trying to predict the weather based on a coin flip.

So, What's the Real Story?

This pre-Thanksgiving dip in mortgage rates is, at best, a temporary reprieve. The underlying economic conditions suggest continued volatility and potential upward pressure on rates in the near future. Don't let the holiday cheer fool you.